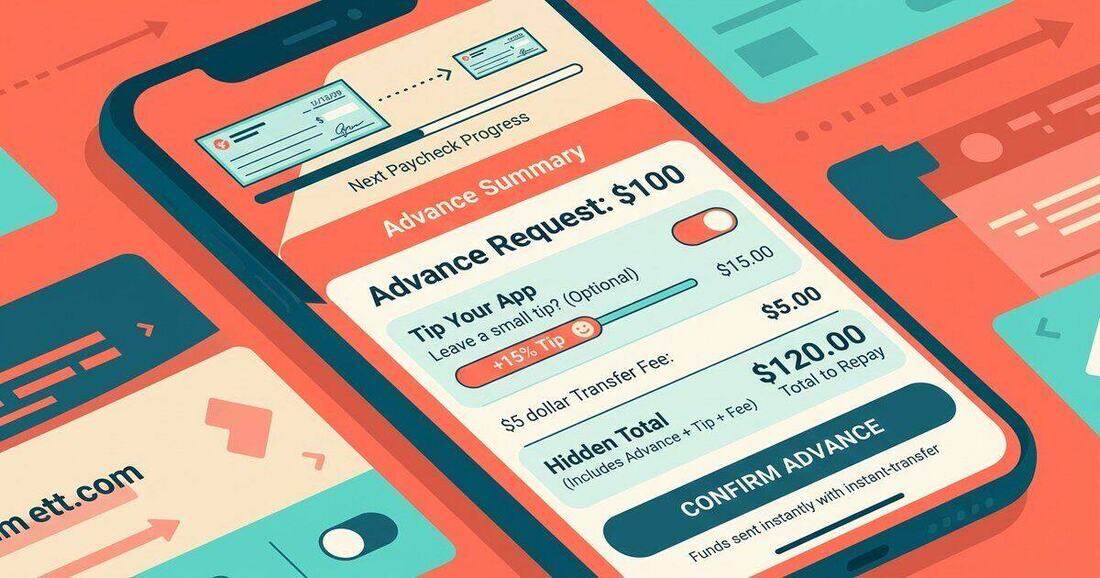

The app says it is free. You link your bank, ask for $100 of pay you have already earned, and a screen pops up: a small "tip" is pre-selected, and there is a $5 charge if you want the money now instead of in a few business days. You are living paycheck to paycheck, so of course you want it now, and turning off the tip feels a little rotten. You pay both. And just like that, "free" cost you eight dollars to borrow a hundred of your own money for a week.

I spent fifteen years in consumer lending, and I want to show you what that eight dollars actually is when you do the math the way a lender would. These apps are not charities. They have a revenue model, and that model is the "tip" and the "instant" fee you barely noticed.

"It's free, right?" The question every cash advance app wants you to stop asking

The marketing leans hard on "no interest, no mandatory fee." Technically true, and beside the point. The money is made on the parts that are framed as optional or as a convenience, and most people pay them.

The CFPB studied this market and found that despite the free framing, about 90% of workers paid at least one fee, and the great majority of all fees paid were for expedited, instant access to the money. The average advance was just $106, workers took about 27 advances a year, and the fees came to roughly $68.88 per worker per year. (Those are 2022 figures, the most recent in the CFPB's data, so read them as the pattern, not a 2026 count.) "Free" is the headline. The fee is the business.

How these apps actually make money

Two levers, and they work together.

The first is the express, or instant, fee, usually a few dollars to move your advance to your account immediately instead of waiting a couple of days. The CFPB found this is where almost all the fee revenue comes from, because when you are short on money you generally cannot wait. The second is the "tip," a suggested gratuity that is often pre-selected at checkout, sometimes set to something like 15% of the advance by default. You feel like a cheapskate for removing it, which is precisely the design. Stack the express fee and the tip together and you have the real price of the advance, even though neither one is called interest.

The math: turning a $3 fee and a 15% "tip" into a real APR

Here is where it stops being abstract. A small fee on a small advance for a short time annualizes into a number that will stop you cold.

The CFPB ran these illustrative examples, and they are worth seeing in full:

- A $106 advance with a $3.18 fee over a 10-day term works out to a 109.5% APR (the employer-partnered example).

- A $50 advance with the same $3.18 fee over just 4 days works out to a 580.4% APR.

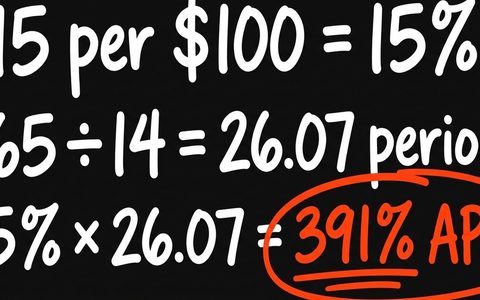

- A $144 advance over 7 days with $8 in combined average tip and fee works out to 290% APR (a direct-to-consumer example).

The pattern is the same one that makes payday loans so expensive: a small charge over a very short term is a large cost per year. The shorter the advance and the smaller the amount, the higher the effective APR, because the fee is a fixed cost spread across very few days. These are calculations, not rates the apps disclose, which is exactly the point. The cost is real; it just never appears as a percentage on your screen. The same arithmetic drives the hidden APR of a payday loan.

Why the "tip" isn't a tip

A tip implies a gratuity, optional, going to a person, on top of a fair price. That framing does a lot of work to make this feel friendly. The numbers tell a different story.

Dave, one of the larger apps, reported about $62 million in "tips" in 2022, per its own SEC filing as cited by federal regulators. Sixty-two million dollars is not gratitude. It is core revenue dressed in friendlier clothes.

The FTC took action on this. In November 2024 it sued Dave, alleging the app marketed advances "up to $500" that it rarely actually offered, charged an undisclosed "Express Fee," and applied a default 15% "tip" without clear consent. The FTC also alleged that the company's charitable framing was misleading: that for each percentage point of "tip," Dave donated about ten cents to a meal program and kept the rest. One consumer the FTC cited said the interface "is set up to trick you into giving the tip" and that they felt "cheated/scammed." These are allegations in an ongoing matter, not a final judgment, so I am stating them as the FTC's complaint, not settled fact. But the pattern they describe is one worth recognizing before you tap "confirm."

What changed in 2026, and why no app is required to show you an APR now

This is the part that matters most for your wallet today. The rules just shifted in the apps' favor.

In late December 2025, the CFPB concluded that certain earned-wage-access products are not "credit" under the Truth in Lending Act, withdrawing an earlier proposed rule that would have treated them as loans requiring loan-style disclosures. In plain terms: in 2026, many of these apps are not required to show you an APR. The burden of seeing the real cost is back on you.

That position has flip-flopped more than once in recent years and remains contested, so treat it as the current state rather than something settled forever. The CFPB's "covered" definition does describe a lower-risk model worth knowing: no required fee, no recourse or collections, no credit reporting, an advance no larger than wages you have already earned, often through payroll deduction. An app that fits that mold and charges you nothing to wait is genuinely low-risk. An app leaning on express fees and pre-selected tips is the one to scrutinize, and now you usually have to scrutinize it without an APR to guide you.

When a cash advance app is fine, and when it's a trap

Let me be fair, because these apps are not all bad. Used once, to dodge a $35 overdraft fee on a genuinely one-time gap, an app that charges you a couple of dollars can come out ahead. The reader who said "it saved me from an overdraft fee twice" is not wrong about that.

The trap is the next sentence that reader almost always adds: "but then I needed it every single payday." Here is the mechanism. Every advance shrinks your next paycheck by the amount you pulled forward, plus the fees. So next payday you are a little shorter than before, which makes the advance more tempting, which shrinks the paycheck after that. The app becomes a small tax on every check, paid in fees, forever. One-time bridge: sometimes fine. Standing habit: a cycle that quietly costs you more than the overdraft you were avoiding.

Cheaper or safer ways to bridge a gap

If you find yourself reaching for an advance every payday, that is the signal to find a structurally cheaper option. A federal credit union's Payday Alternative Loan caps interest at 28% plus an application fee of no more than $20, bans rollovers, and gives you a fixed payoff instead of an open-ended dependency. A small personal loan may also cost far less per dollar than a string of advances. And if the deeper problem is a thin buffer, our guide to building an emergency fund shows how to start one even on a tight budget.

If you want to see options that come with an actual disclosed APR you can compare, you can see what loan options may be available with no obligation. Our three-way look at credit unions, online lenders, and cash advance apps lays out the cost-versus-speed trade-off.

American Cash Relief is not a lender. This is education, not financial advice, and the effective APR figures here are CFPB illustrations, not rates any particular app quotes, which is the whole reason the math matters: when no one is required to show you the number, you have to find it yourself.

Frequently Asked Questions

Are cash advance apps a loan?

It depends on the model and, as of late 2025, on regulation. The CFPB has determined that many earned-wage-access products are not "credit" under the Truth in Lending Act, so they are often not treated as loans and generally do not disclose an APR, even though the fees behave like the cost of borrowing.

Do cash advance apps affect your credit?

Most do not report to the credit bureaus, so a typical advance neither builds nor harms your credit. The flip side is that responsible repayment usually does not help your score either. Confirm each app's policy, since practices vary.

Can you skip the tip?

Usually yes. The "tip" is presented as optional, often pre-selected at a default like 15%, and you can typically lower or remove it. The interface is frequently designed to make skipping it feel uncomfortable, which is part of why the FTC raised concerns about how these tips are charged.

Why do small app fees add up to such high APRs?

APR expresses cost per year. A few dollars charged on a small advance over just a handful of days, when annualized, can reach well into the triple digits, by the CFPB's own examples (from about 109.5% up to 580%). The short term and small amount are what inflate the rate.

Are cash advance apps worth it?

For a rare, one-time gap, a low-fee advance can beat a $35 overdraft. As a repeated habit, it tends to cost more than alternatives like a credit-union Payday Alternative Loan or a small personal loan, because each advance shrinks your next paycheck and pulls you back for another. The honest test is whether you can use it once and stop.

Need cash before payday?

Pick your amount and get matched with lenders in our network. It's free, secure, and there's no obligation.