Someone at the counter tells you it is "just fifteen bucks per hundred." You need $300 to get to payday, so that is $45. Forty-five dollars to bridge two weeks does not sound like the end of the world. And that framing, the small flat fee, is the whole trick. It hides the real number, and the real number is one of the highest costs of borrowing in the entire consumer market.

I spent fifteen years in lending, and the math here is not complicated. It is just never shown to you at the counter. So let me show it. By the end, you will be able to turn any "$X per $100" payday fee into the APR it actually is, in your head.

"$15 per $100" sounds harmless. Here is what it actually is

That $15-per-$100 fee, on a two-week loan, works out to an APR of almost 400%. That is the CFPB's own number, in the CFPB's own words. Not 15%. Almost four hundred percent a year.

The fee feels small because it is dressed as a flat dollar amount over a short window. The moment you express it the way every other loan is expressed, as a yearly rate, it stops looking harmless. The fee did not change. The framing did. Let me walk the arithmetic so you can see exactly where 400% comes from.

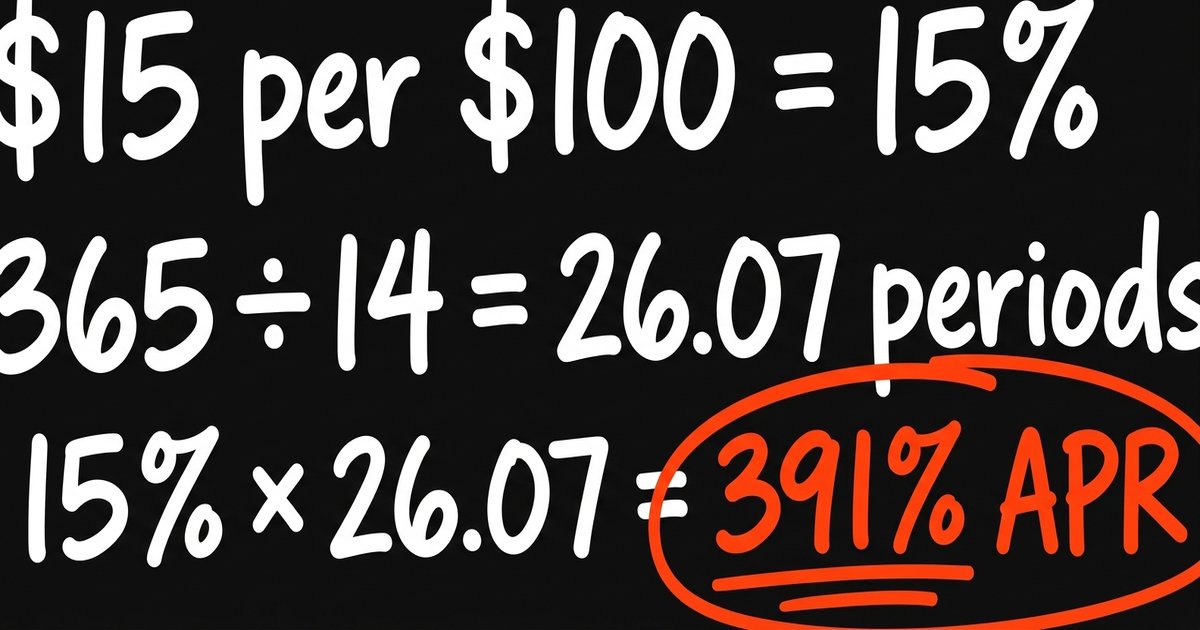

The math, step by step

This is the load-bearing part of the article, and it is just three lines.

- Step 1. $15 fee on $100 borrowed is 15% for the period of the loan. The period is 14 days.

- Step 2. A year has 365 days. Divide by 14 and you get about 26.07 two-week periods in a year. (365 divided by 14 is about 26.07.)

- Step 3. Multiply the per-period cost by the number of periods: 15% times 26.07 is about 391%.

That is your "almost 400 percent." The whole magic trick is the short term. A 15% charge would be ordinary if it covered a year. Charged every two weeks instead, it stacks up more than 26 times over, and that is what the APR captures.

The same method works on any fee. At the low end of the typical range, $10 per $100, the APR lands around 260%. At the high end, $30 per $100, it roughly doubles the common case to about 782%. The finance charge can range from $10 to $30 for every $100 borrowed depending on your state, so the APR moves with it. The fee on the wall is small. The annual rate is not. You can run any fee and term through our payday loan APR calculator to see the real number in seconds.

Why APR is the only fair way to compare

You might ask why we bother annualizing a two-week loan at all. Because APR is the one number that lets you put unlike loans side by side.

A credit card might charge 24% APR. A payday loan's "$15 per $100" sounds smaller than 24 of anything, until you annualize it and find it is sixteen times higher. Without APR, you are comparing a flat fee to a yearly rate, which is comparing apples to a calendar. APR converts every loan to the same yardstick, cost per year per dollar borrowed. That is exactly why the Truth in Lending Act requires payday lenders to disclose it: so you can see the real number on the agreement, even when the person at the counter only says "fifteen bucks." Look for it on your paperwork. It is there.

The part lenders don't show you: rollovers

Even 391% understates the danger, because that figure assumes you pay the loan off on time, in one shot. Most people don't.

Here is how it compounds. You borrow $300 and owe $345 in two weeks. Payday comes and you cannot spare the full $345, so you roll it over: pay another $45 fee to push the due date out two more weeks. The principal, the $300, has not moved an inch. Four weeks of rollover means $90 in fees on $300 borrowed, and you still owe the original $300. The fee meter runs while the debt stands still.

That is the mechanism. It is not a rare accident. The CFPB's overview of how payday loans work describes exactly this renewal cycle as the central risk. It is the most common path a payday loan takes.

How a "two-week loan" becomes a five-month debt

The data on this is stark, and it comes from the regulator, not from me. The CFPB has found that the large majority of payday loans are rolled over or renewed within two weeks, and that most borrowers who rolled over owed as much or more on their final loan in the sequence as they did at the start. A meaningful share of borrowers on a monthly schedule stayed in debt the entire year of the study.

This is the reader who said, "It was just supposed to be a quick $300 until payday. Six months later I was still paying it." And the one who said, "I went to a second lender to pay the first, then a third to pay the second." Those are not horror stories from the edges. They describe the typical arc. The FDIC and other regulators have pushed banks and credit unions to offer affordable small-dollar alternatives precisely because the payday cycle is so well documented (see the FDIC Consumer Resource Center).

See your own number

The fee they quote you is designed to feel small. The way to break that spell is to run your own loan through the same three steps: per-period cost, number of periods in a year, multiply. If you would rather not do it by hand, our true-cost calculator turns any "$X per $100" and term into the APR and the total you would actually pay, including what a rollover or two adds. Seeing your own number, in your own dollars, tends to make the decision for you.

Cheaper lanes for the same emergency

If you are weighing a payday loan this week, know that there are far cheaper ways to cover the same gap. A federal credit union's Payday Alternative Loan caps interest at 28% plus an application fee of no more than $20, and rollovers are prohibited by rule, so the trap that does the real damage simply cannot form. Small installment loans and other options may also beat payday on cost.

If you want to see options that will not annualize into the triple digits, you can see what loan options may be available with no obligation. For a fuller head-to-head, our comparison of a personal loan versus a payday loan runs the same need through both products, and our guide to credit unions, online lenders, and cash advance apps shows where to look first for fast cash.

One last reminder: state law varies dramatically here. Some states ban payday lending outright, others cap rates or limit rollovers, so costs and legality depend on where you live. None of this is financial advice, and American Cash Relief is not a lender and not a payday lender. It is an explanation of a number that is too often kept out of view.

Frequently Asked Questions

Is a 400% APR even legal?

It depends on your state. Some states ban payday lending, others cap rates or limit rollovers, and in states that permit it, fees equivalent to roughly 400% APR are legal. The lender must still disclose the APR under the Truth in Lending Act, so the real number is on your agreement.

Why is the payday APR so much higher than the "interest rate" they mention?

Because the fee is charged over a very short term, usually two weeks, and APR expresses it as a yearly cost. A 15% charge every two weeks repeats more than 26 times in a year, which is what pushes the annual rate near 400%.

How do I convert a "$15 per $100" fee to an APR myself?

Three steps: the fee as a percentage of the amount (here, 15%), times the number of loan periods in a year (365 divided by 14 is about 26.07 two-week periods), gives roughly 391%. Swap in your own fee and term to get your number.

What does a rollover actually add?

Each rollover charges a fresh fee while leaving the principal untouched. Rolling a $300 loan for four weeks adds about $90 in fees, and you still owe the original $300. Most payday loans get rolled over or renewed, which is how a two-week loan becomes a months-long debt.

Is there a cheaper option for the same emergency?

Often yes. A credit-union Payday Alternative Loan caps interest at 28% plus up to a $20 fee and bans rollovers. Small installment loans may also cost far less. Both let the debt actually end instead of cycling.

Need cash before payday?

Pick your amount and get matched with lenders in our network. It's free, secure, and there's no obligation.